Tax Cuts and Jobs Act of 2017: What Taxpayers Need to Know

On December 22, 2017, President Trump signed the Tax Cuts and Jobs Act of 2017 (the act or TCJA). The legislation makes significant changes to the Internal Revenue Code (IRC), including individual, corporate, and gift and estate taxation.

Individual income tax changes

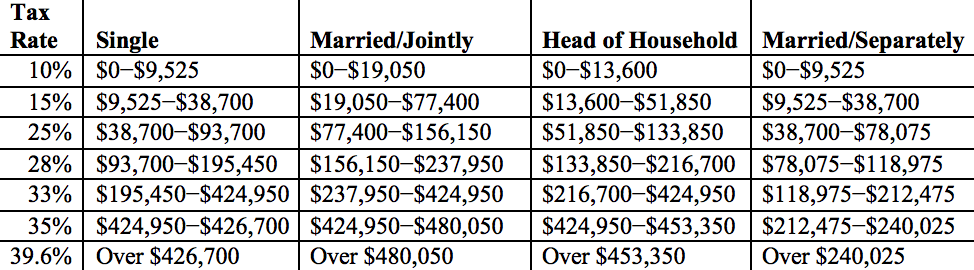

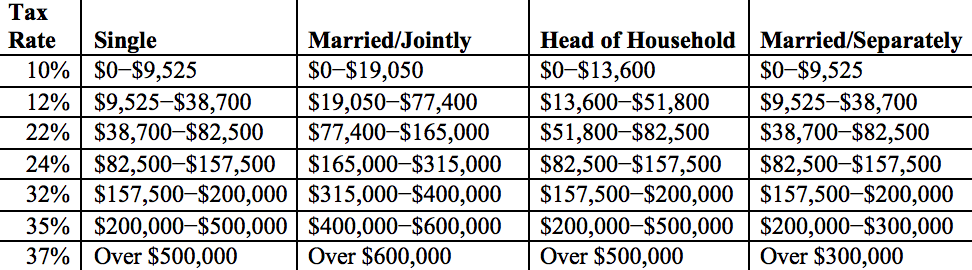

Although the act maintains seven tax brackets, these brackets have changed.

Current tax rates

New tax rates under the TCJA

In addition to the changes made to the tax brackets, many exemptions and deductions for individual income tax have been repealed or modified.

• The personal exemption of $4,150 per taxpayer and dependent has been eliminated.

• The standard deduction for individuals has gone from $6,500 for individual taxpayers and $13,000 for married couples who file jointly to $12,000 for individual taxpayers and $24,000 for married couples who file jointly. This near doubling of the standard deduction will result in more taxpayers taking this deduction instead of itemizing.

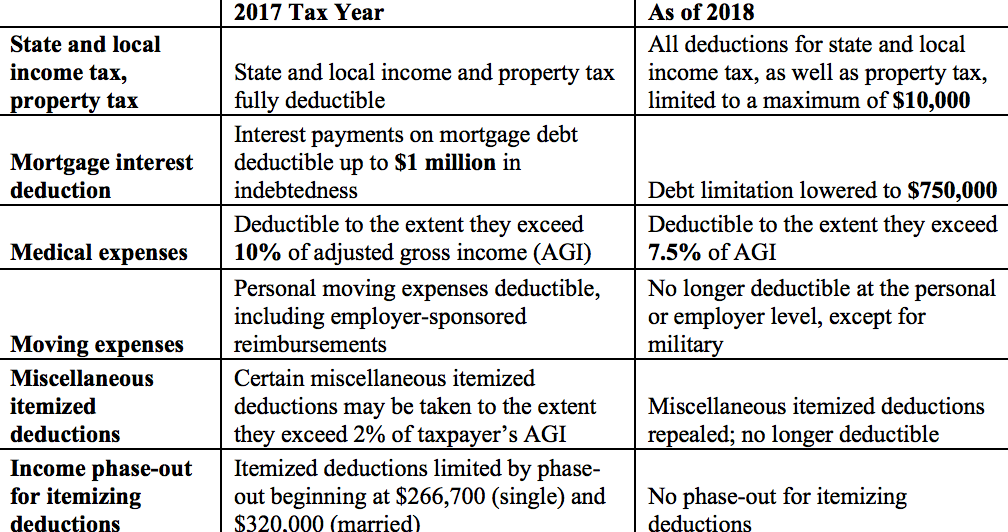

• The legislation also places limits on several itemized deductions, listed in the table below.

Specific itemized deductions that have been eliminated or modified

Miscellaneous individual income tax changes

In addition to the major modifications discussed above, several other changes in the bill may affect your financial decisions going forward. These are:

Family tax credits.

The child tax credit has been doubled, from $1,000 to $2,000, and the refundable portion of that credit is allowable up to $1,400. The act also grants a new credit of $500 for other dependents. These will phase out at income limits of $200,000 (single) and $400,000 (married).

Estate and gift taxes.

Effective January 1, 2018, the individual unified gift and estate tax exemption has been raised to $11.2 million (up from what was set to be $5.6 million) and, with portability remaining intact, $22.4 million for a married couple. The top rate will remain 40 percent. The new rates are set to expire—and return to 2017 levels—at the end of calendar year 2025.

Cash donations to charity.

Under 2017 law, gifts of cash to charity offered a taxpayer the ability to deduct the contribution, up to 50 percent of AGI. The TCJA has increased the limitation to 60 percent of the taxpayer’s AGI.

Education planning.

The TCJA includes an expansion of 529 savings plans that allows families to save for K−12 expenses, in addition to college expenses. 529 plans will also be able to use qualified distributions for elementary and secondary school expenses, up to $10,000 per year, per student.

1031 exchanges.

Beginning January 1, 2018, 1031 exchanges have been limited to real property.

Affordable Care Act individual mandate.

The TCJA eliminates the penalty imposed under the IRC for individuals who do not maintain individual health care coverage.

Individual alternative minimum tax (AMT).

The individual AMT exemption amount has increased to $70,300 for individual filers and $109,400 for joint filers. The phase-out for the AMT exemption has increased to $500,000 for individuals and $1 million for married couples. With enactment of the new act, fewer Americans will be subject to the AMT.

Retirement recharacterizations.

The TCJA eliminates the ability for a taxpayer to unwind a Roth conversion and “recharacterize” back to a traditional IRA. This applies to conversions occurring after January 1, 2018. Be sure to speak with our office before considering any new recharacterizations, as there is current debate as to whether Roth conversions that occurred in 2017 may still be characterized in 2018.

Pass-through business income.

Under law in effect for the 2017 tax year, all pass-through business income is taxed at the individual taxpayer’s marginal rate, as is most ordinary income. Under the TCJA, qualified pass-through business income will be addressed in a new IRC Section 199A as follows:

- Deduction of 20 percent of the non-wage allocation of qualified business income from the trade or business

- Deduction limited to 50 percent of W-2 wage income (The limitation was set in an effort to prevent abuse in classifying wage income as business income in order to receive a lower rate for income that should be taxed at ordinary income rates.):

- For individuals: Income earned over $157,000

- For married couples: Income earned over $315,000

- Certain service professionals (e.g., attorneys, accountants, financial professionals): Excluded from taking the deduction for income above $157,000 for an individual and $315,000 for a married couple.

Please note: The changes to pass-through business income taxation sunset at the end of calendar year 2025, as written in the TCJA.

Corporate taxation

Although the changes to how individual income is taxed are set to expire at the end of 2025, the corporate tax changes provided for in the TCJA will be permanent. One of the largest tax cuts in the legislation lowers the corporate tax rate from 35 percent to 21 percent, effective January 1, 2018. Furthermore, the TCJA completely repeals the corporate AMT. The act also imposes some limitations on certain corporate tax deductions, including those for net operating loss, business interest, and R&D expenditures.

Year-end tax planning strategies in light of reform

There is still a bit of time to take advantage of strategies that may positively impact your 2018 tax bills. These strategies may or may not be available to every taxpayer, though it is important to consider them and how they may work for you. As always, we recommend that you speak with your accountants and tax preparers as soon as possible about the viability of any of these actions.

Prepay property tax

If possible, you may want to consider making prepayments of property taxes that would have otherwise been paid in 2018. But be sure to consult your tax professional before doing that for any state income tax that you estimate for 2018. The final version of the TCJA contains a clause that will not allow for the deductibility of state and local income taxes prepaid in 2017 that would otherwise be assessed and due in 2018.

Marginal rate review

Review significant changes in marginal tax rate at the federal level for the possibility of deferring income where possible and perhaps delaying the sales of large assets. In some cases, the acceleration of income may help taxpayers with large families and who would lose out on some significant tax savings garnered from the family-friendly personal exemption.

Accelerate deductions

One possible tax-relieving strategy is to accelerate deductions that are disallowed in 2018. This is especially true for taxpayers who itemize deductions. Some examples of ways to do this include making an extra mortgage payment or making additional charitable donations. This is not viable for every taxpayer, however; for some, making these deductions in 2018 will bring the dollar amount of the items above the new standard deduction figure.

For any of these strategies, it is imperative for you to analyze your tax picture for 2017 and 2018 in the hope of taking steps that will result in the most tax savings.

Assess where you are headed

In light of these sweeping changes, 2018 should result in a complete review of your financial snapshots. An overall review of income, assets, and balance sheet is important in order to get a clear picture of how the significant changes to individual income taxation will affect you and your family.

More planning opportunities will continue to arise as the new tax code unfolds. Please reach out to our office so we can help you navigate these changes and answer any questions you may have.

This material has been provided for general informational purposes only and does not constitute either tax or legal advice. Although we go to great lengths to make sure our information is accurate and useful, we recommend you consult a tax preparer, professional tax advisor, or lawyer.